Colombian payments: an evolution

Payment methods have evolved significantly in Colombia's economic landscape, adapting to the changing needs and preferences of the population. From traditional cash and check payments to innovative digital solutions, Colombians today have a wide range of options for conducting financial transactions.

This guide provides a comprehensive and detailed overview of payment methods in Colombia, highlighting traditional approaches and emerging technologies that are transforming the way money is managed in the country.

Is Cash Still King?

The use of cash in Colombia remains significant, although it has undergone significant changes due to the increasing adoption of digital payment methods and government policies aimed at promoting financial inclusion and reducing cash usage.

In terms of the number of transactions nationwide, cash was the most used medium in 2023 (78.4%), followed by electronic transfers (12.6%), debit cards (7.9%), and credit cards (1.2%).

Looking specifically at cities, Bogotá stands out for lower cash usage and higher adoption of electronic transfers. In contrast, in Cali, Medellín, and Barranquilla, cash usage is considerably higher, while debit cards and electronic transfers are used less.

Those who prefer cash often do so to avoid additional costs associated with traditional digital payments, such as fees for transfers between different banks and charges for the use of POS terminals. These costs can affect profit margins, especially in businesses with tight margins.

This pain point has accelerated the arrival of fintechs to the country's financial landscape, aiming to digitize cash transactions. This trend is due to the growing demand for alternatives that counteract the high costs and limitations of traditional banks. Over time, cash is being relegated to the background more and more as the population adopts more efficient and cost-effective financial solutions.

Checks and Bank Transfers

Although digital payment methods have experienced significant growth in Colombia, checks and bank transfers remain an integral part of the payment landscape in the country, especially in high-value commercial transactions and the business sector.

Although the use of checks has declined over time due to digitization, they are still used by some companies and individuals to make important payments. According to recent data from the Banco de la República, approximately 3.5 million check transactions were recorded in Colombia in 2023, representing 12% of non-monetary transactions.

On the other hand, electronic bank transfers have maintained their relevance in the Colombian market. In 2023, over 120 million electronic transfers were made, with a total value of more than 250 trillion Colombian pesos, according to statistics from the Financial Superintendence of Colombia. This payment method is widely used in commercial transactions, bill payments, and fund transfers between individuals.

ACH Colombia

ACH Colombia, or Automated Clearing House Colombia, is an entity that facilitates electronic transactions between different banks and financial institutions in the country. Its main function is to process payments and interbank transfers efficiently and securely. This includes a variety of services, such as bank transfers, payroll payments, and utility bill payments.

ACH Colombia operates based on a technological infrastructure that connects the systems of different banks, allowing transactions to be carried out automatically. This process ensures that transfers are completed correctly and that funds reach their destination without issues.

ACH Colombia is efficient in processing transactions, which can reduce the time it takes to complete an interbank transfer. However, it's important to note that this service can incur certain costs for the banks, which might sometimes be passed on to the end users. Additionally, relying on a robust technological infrastructure and coordinating between multiple entities can present challenges.

In terms of transaction times, transfers through ACH Colombia are usually completed within one business day. However, depending on the agreements between the financial entities involved, some transactions might be processed more quickly.

Transfiya

Transfiya is an online money transfer service supported by ACH Colombia. It makes it easy to send, receive, and request money between users of different banks in Colombia, using only a cellphone number.

To use Transfiya, both the sender and the recipient need to have accounts with one of the financial institutions that support the service, currently around 18 in total. Users must register their phone number with the relevant banking app. To send money, users need only the recipient's phone number, making the transfer quick and simple. The recipient gets a notification, and if they have only one registered bank account, the money is deposited automatically. If they have multiple accounts, they can choose which one to receive the funds into.

The main advantages of Transfiya include the immediacy of transactions, which are completed in seconds, and the simplicity of the process. Additionally, Transfiya is available 24/7, and transactions are free for users.

However, Transfiya has some limits, such as a maximum of COP 3,000,000 per day and up to 15 transactions daily. Also, while it is compatible with many banks, not all banks in Colombia are integrated into the system, which may limit its use for some users.

PSE: Online Secure Payments System in Colombia

PSE, known as Secure Online Payment, is an electronic payment method offered by ACH Colombia that continues to be a traditional option in the Colombian banking system. It allows users to make purchases and payments online, debiting money directly from their bank accounts, whether savings, current, or electronic deposits.

Despite its convenience and widespread use, PSE has some disadvantages. One of them is that it requires the user to have a bank account, excluding those who do not have access to formal financial services. Additionally, the registration and setup process may be complicated for some users less familiar with technology.

Despite these limitations, PSE remains a popular choice for conducting online transactions in Colombia. It is especially used by companies and merchants who want to offer their customers a secure and reliable way to make online payments. Although a wide range of more advanced and modern electronic payment options has emerged, PSE continues to be a reliable and widely accepted option in the country.

Efecty

Efecty is a Colombian company that offers money collection services, payments for multiple services, and national and international money transfers.

How Does Efecty Work?

To send national transfers in person, you only need to present a valid identification document, confirm the recipient's details, and hand over the cash. Minors cannot make transfers.

International Transfers

Efecty also allows you to send and receive international transfers thanks to its agreement with Western Union. These transfers can be processed at Efecty's service points or at allied bank correspondents. To receive or send international transfers, you need to present a valid identification document. When receiving money from abroad, the amount is delivered in Colombian pesos, as the country's regulations do not allow receiving the original currency sent.

Efecty Fees

Efecty does not charge for receiving national or international transfers, but it is important to note that Efecty and Western Union do not use the average market exchange rate, but their own exchange rate, which generally includes a hidden surcharge. This surcharge may result in receiving less money than expected when converting foreign currency.

Neobanks: Innovation in the Colombian Financial Sector

Neobanks have emerged as an innovative alternative in the Colombian financial sector, offering accessible and affordable digital banking services that benefit especially people and communities that have traditionally been underserved by conventional banks.

Cost Reduction and Improved Access

In a country where a large portion of the population lacks access to traditional banking services due to high costs and lack of banking infrastructure in rural areas, neobanks represent a viable solution to improve financial inclusion. Neobanks like Nequi, Daviplata, Lulo Bank, Nu, and RappiPay have gained popularity due to their fee-free services and ease of use.

Ease of Use and User Experience

With user-friendly mobile applications, neobanks allow Colombians to manage their finances conveniently from their smartphones. This is particularly beneficial in a country where smartphone penetration is constantly increasing, making it easier for more people, including those in rural areas, to access banking services without the need to travel long distances to a physical branch.

Fintechs

Colombia is a hotbed for emerging fintechs that facilitate access to financial services and promote financial inclusion.

Accessibility and Customization

Fintechs use technology to offer more accessible and personalized financial services. For example, some fintechs specialize in offering microloans through digital platforms, which is crucial for small business owners and informal workers who have traditionally struggled to access credit through conventional banks. This not only helps drive the growth of small businesses but also contributes to job creation and local economic development.

Innovation and Competition

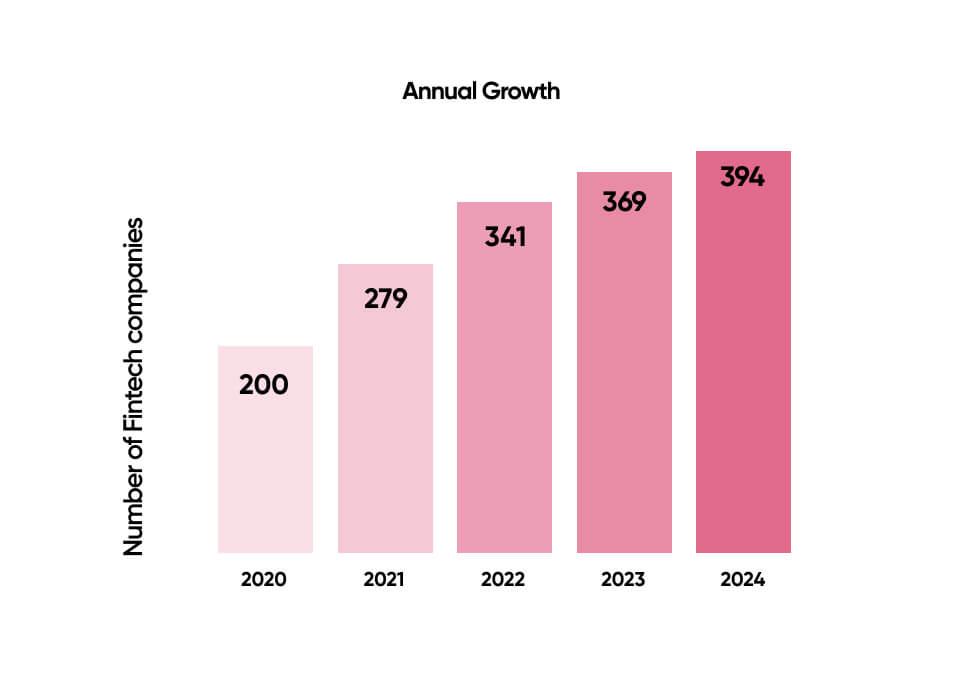

By introducing new business models and technologies, fintechs foster competition in the financial sector. As of April 2024, the number of local fintech companies in Colombia stands at 394, reflecting a 6.8% growth in the ecosystem over the past year. This growth not only demonstrates the vitality and dynamism of the sector but also its ability to attract investment and talent. Fintechs in Colombia are diversifying and encompassing a wide range of services, from digital payments to loans, investment management, and insurance.

Benefits of Fintechs for Colombians

The expansion of fintechs in Colombia offers numerous benefits to consumers:

- Cost reduction: Fintechs, by operating mainly online, can offer services at lower costs than traditional banks, which is especially beneficial for small and medium-sized enterprises (SMEs) and informal workers.

- Expanded access: Fintechs help financially include people and communities that have historically been underserved by the traditional banking system. Through accessible and easy-to-use platforms, more Colombians can access essential financial services.

- Innovation and customization: Fintechs are at the forefront of financial innovation, offering personalized products that cater to users' specific needs, such as microloans, digital payments and financial management tools.

- Security and efficiency: Fintech solutions often incorporate advanced security technologies and offer greater efficiency in managing personal and business finances.

Virtual Wallets

Virtual wallets have gained popularity in Colombia and are also playing a crucial role in transitioning to a more digitized economy.

Ease of Use and Expanded Access

Virtual wallets allow users to store and manage funds electronically, simplifying payments and transfers. This is especially useful in the Colombian context, where many informal workers and small businesses need quick and accessible solutions to manage their daily finances. The ease of downloading an app and getting started reduces entry barriers for those not familiar with traditional banking services. The preferred ones by Colombians are Nequi, Daviplata, Bancolombia App, Mercado Pago, and Wompi, due to their ease of use and wide acceptance network in commerce and services. Other virtual wallets like RappiPay and Movii are also gaining ground due to their cashback offers and promotions.

Cross-Border Payments

According to recent data from the World Bank, an estimated 40% of businesses in Colombia are involved in import and export activities, highlighting the importance of efficient solutions for cross-border payments.

Traditional methods of transferring money to other countries can be slow, expensive, and complicated. Fintechs are addressing these issues by offering more efficient and affordable cross-border payment solutions. It is estimated that over 60% of SMEs in Colombia have used some form of fintech service for cross-border payments in the past year.

Fintechs specializing in international payments use advanced technology to offer fast, secure transfers with lower costs than traditional financial institutions. Platforms like Wise, WorldRemit, and Conduit allow Colombian companies to send and receive money in multiple currencies with competitive exchange rates and reduced fees.

A Regional Role Model

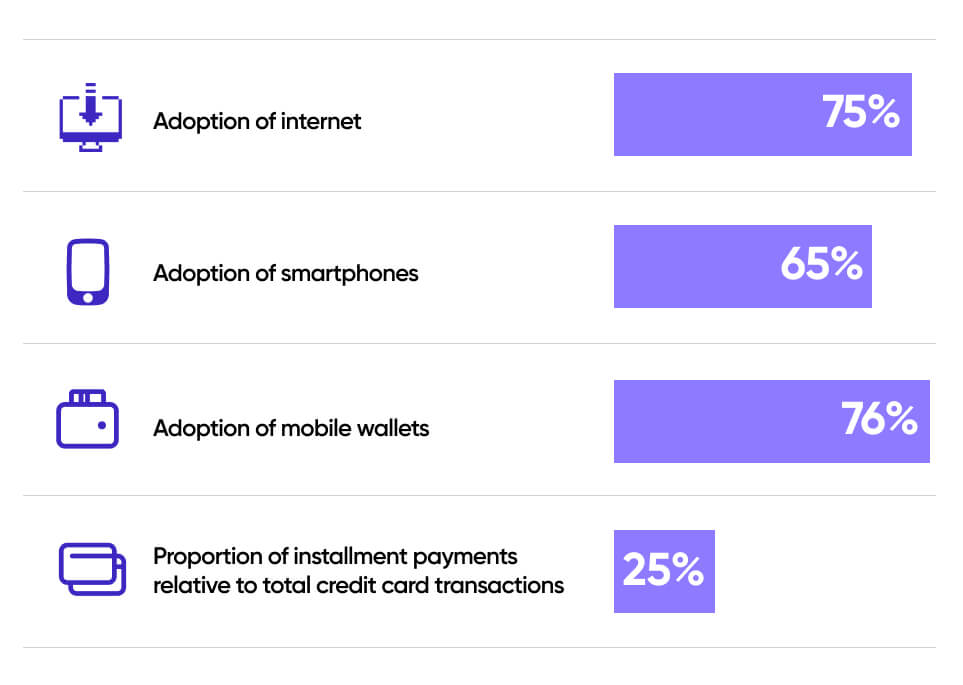

Colombia has stood out in Latin America for its rapid adoption of digitization in the financial sector. According to recent data, it is estimated that over 60% of the Colombian population has access to financial services via mobile devices, demonstrating a high presence of technology in citizens'

daily lives.

Compared to other countries in the region, Colombia is in a favorable position in terms of fintech adoption. According to a report by the Inter-American Development Bank (IDB), Colombia ranks third in Latin America in terms of financial inclusion, with a financial services usage index of 68%, surpassed only by Brazil and Chile.

This advancement in financial digitization has been driven by several factors, such as the increasing presence of smartphones, the development of telecommunications infrastructure, and government support for financial inclusion initiatives.

Additionally, the fintech ecosystem in Colombia has experienced significant growth in recent years, with a 36% increase in the creation of new fintech companies in 2023. This growth reflects investor confidence and entrepreneur interest in the Colombian fintech market.

In summary, Colombia is in a prominent position in the adoption of digitization in the financial sector in Latin America, with a high level of usage of digital financial services and a growing fintech ecosystem. This progress not only drives economic development and financial inclusion in the country but also strengthens Colombia's competitiveness on the regional and global stage.

The Future of Payments in Colombia

The continued growth of fintechs and the adoption of their services by SMEs suggest an exciting future for payments in Colombia. Increased adoption of digital payments is expected as a result of growing technological infrastructure and widespread internet access. This trend will go hand in hand with the development of an instant payment infrastructure, facilitating fast and efficient transfers.

The Colombian financial landscape will also see significant growth in fintechs and neobanks, offering a wide range of innovative services and challenging the dominance of traditional banks. Competition among financial service providers will drive innovation and continuous improvement in the user experience.

Financial security will be a priority in this evolving digital environment, with a focus on strengthening security measures and protecting users' personal and financial information.

With the increasing integration of digital solutions into the country's economy, we can anticipate that payments will become more accessible, faster, and more affordable for all Colombians. This transformation will not only drive economic growth but also strengthen Colombia's competitiveness on the global stage.