What is ACH?

ACH (Automated Clearing House) is an electronic payment system that facilitates financial transactions between bank accounts in the US and abroad. The ACH network enables transactions such as direct deposits, electronic bill payments, business-to-business payments, e-commerce payments, and person-to-person payments.

What is a clearing house? A clearinghouse is a designated intermediary between a buyer and seller in a financial market. The clearinghouse validates and finalizes the transaction, ensuring that both the buyer and the seller honor their contractual obligations.

ACH, which is managed by Nacha, was officially established in the mid-1970s. Since then, it has become a widely used system in the US, processing large volumes of transactions daily.

What is an ACH payment?

An ACH payment is an electronic money transfer which is sent between banks using the ACH Network, a system that batches and processes these transactions.

How ACH Payment Transactions work

ACH transfers operate on a batch processing system, not a real-time one. This means banks and financial institutions collect and store payment instructions from senders throughout the day. Then, these instructions are sent electronically as a batch to other financial institutions.

A typical ACH transaction may look like this:

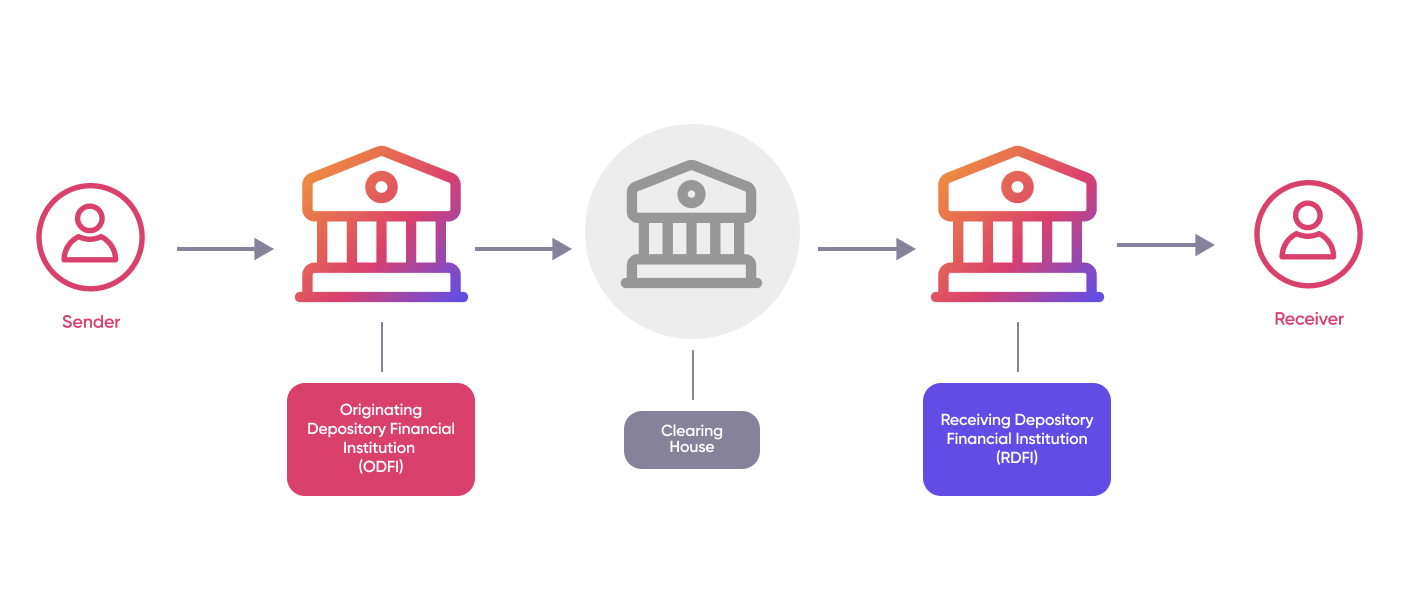

- A person, business, or government agency starts a transfer through the ACH network.

- The sender's bank (called the Originating Depository Financial Institution) transmits the ACH transfer details to one of two central clearing facilities: The Federal Reserve or The Clearing House.

- The clearing facility sorts the ACH transfer data and sends it to the recipient banks (known as Receiving Depository Financial Institutions) specified in the transfers.

- The recipient banks then adjust the accounts of the people or businesses involved in each ACH transfer by either debiting or crediting them.

Once received, each ACH transfer typically settles within one to two days for credits and one business day for debits. This means the transfer of information happens quickly, usually on the same day, but the actual movement of funds into accounts may take several days.

Sending money with ACH

To complete an ACH transfer, you'll need the name of the account holder, the routing number, the ABA number, the account number, and the amount you want to transfer.

Understanding ABA Numbers The ABA number, or American Bankers Association number, is a nine-digit code that identifies banks in the United States.

Types of ACH Payments

The ACH Network handles two types of transactions: direct deposits and direct payments.

1. Direct Deposits: These are electronic transfers initiated by a business or government entity to deposit funds directly into an individual's bank account. Examples include:

- Paychecks

- Government benefits

- Tax refunds

- Annuity payments

- Interest payments

2. Direct Payments: Also known as ACH debits, these transactions allow individuals, businesses, and organizations to initiate electronic payments from their bank accounts to pay bills, make purchases, or transfer funds to other parties. Examples include:

- Online bill payments

- Payments to vendors or suppliers

- Peer to peer transfer through platforms like Venmo or Zelle

Can ACH be used for cross-border payments?

International ACH Transfers, also known as Global or Cross-Border ACH, uses similar systems like ACH in different parts of the world to make global payments from US-based accounts. These systems include EFT in Canada, SEPA in Europe, BACS in the UK, or BECS in Australia.

International ACH Transfer Example: XYZ Company, a manufacturer of electronic gadgets, needs to pay one of its suppliers in Europe. XYZ Company has an account at JPMorgan, a US bank.

XYZ Company creates a payment order for their supplier in Europe. They can check the current exchange rate between dollars and euros before sending the transaction. This ensures that XYZ Company knows the exact amount of money they're sending in USD and how much their supplier will receive in EUR. Once the payment is initiated, XYZ Company can track and reconcile the payment like any other transaction, although the payment itself will be sent from the ACH Network to SEPA.

The time it takes for these transfers to be completed varies, depending on the specific payment system used outside of the US.

How to do an International ACH Payment

Senders can initiate international ACH transfers at banks and money transfer services. However, while most banks typically offer international wire transfers to customers, only a few banks offer global or international ACH transfers to the public. .

Sending money internationally with ACH

Here are the steps required to perform an international ACH transfer:

1. Gather recipient details, including:

- Name

- Address

- Bank account number

- Routing number (or international equivalent)

2. Provide payment details online, over the phone, or in person at a branch.

3. Confirm the amount and currency type.

4. Provide recipient information.

5. Check the cost and estimated arrival time.

6. Confirm the transfer details and send the ACH payment.

How much does an international ACH payment cost?

ACH transfers are among the most affordable ways to send money. While some banks may waive the fee, others may charge up to $3 for domestic payments. Keep in mind that sending money internationally will typically cost more than domestic transfers. Sometimes, you might pay extra to speed up the delivery of your funds.

To find out the fees, check with your bank and compare them with software alternatives. Lower costs mean more opportunities for global networking.

How long does an international ACH payment take?

International ACH transfers usually take 1 to 5 business days, with an average of 3 days. The type of payment also affects how long it takes to deliver funds. Additionally, the recipient's bank may take a day or two to deposit the funds into their account.

Different countries have varying regulations. If your international ACH transfer takes more than 7 business days to reach your recipient's bank, consider contacting customer service for assistance.

International ACH Payments vs. International ACH Transactions (IAT)

International ACH Transactions are not the same thing as International ACH Transfers / Global ACH.

Understanding the distinction between these terms can be a bit complex. The terms International ACH Transfer and Global ACH are often used interchangeably to describe ACH transfers that move money from a US-based bank account to an account in another country and currency.

Meanwhile, an International ACH Transaction (IAT) is an SEC (Standard Entry Class) code that identifies a transaction as a cross-border ACH payment. SEC codes are linked to the ACH payment request and form part of the NACHA file format used for sending or receiving ACH transactions. IAT is utilized for all Global ACH/International ACH Transfers and has replaced previous cross-border SEC codes such as PBR and CBR.

International ACH transactions focus more on reporting than on actually transferring money. When a bank advertises that it offers IATs, it doesn't necessarily mean that individual customers can use the service. Instead, it indicates that the bank meets legal reporting obligations.

ACH Payment Vulnerabilities

Speed

A significant vulnerability of ACH transfers is the time it takes for transactions to process. While ACH transfers are typically cheaper than other forms of electronic funds transfer, such as wire transfers, they often take longer to complete. This delay can be a disadvantage in urgent payment scenarios, where immediate fund availability is crucial.

Fees

While ACH transfers are generally considered cost-effective for both individuals and businesses, they are not entirely fee-free. Financial institutions may charge fees for ACH transfers, which can vary depending on factors such as the type of transaction, the amount transferred, and whether it is a domestic or international transfer. These fees can add up, particularly for businesses conducting a high volume of transactions, and may affect the overall cost-effectiveness of using ACH transfers as a payment method.

Security Concerns

Phishing: Fraudsters may use phishing techniques, such as fake emails or texts, to trick individuals or businesses into revealing sensitive information like account details.

Malware: The risk of malware infecting systems and compromising account information poses a security threat to ACH transfers.

Limited Recourse for Unauthorized Transactions

Compared to credit cards, ACH transfers provide limited recourse for unauthorized transactions. If unauthorized debits occur, it may be more challenging to recover the funds.

Risk of Account Compromise

In cases where an individual's or business's account information is compromised, unauthorized ACH transactions can occur, leading to financial losses.

Lack of Real-Time Confirmation

ACH transfers lack real-time confirmation, making it challenging for senders to immediately verify whether the recipient's account information is accurate or if the transaction was successful.

Dependence on Banking Hours

ACH transfers are typically processed during banking hours. Transactions initiated outside these hours may experience delays, impacting the efficiency of fund transfers.

Potential for Payment Reversals

In certain situations, ACH transactions may be reversed if there are errors or disputes, leading to uncertainties in the completion of payments.

Fraudulent ACH Transactions

Fraudsters may attempt to initiate fraudulent ACH transactions by gaining unauthorized access to bank accounts or using false information, leading to financial losses for the account holder.