Los sistemas de pago internacionales tradicionales están desactualizados

El comercio internacional depende de la eficiencia y confiabilidad de los pagos. Sin embargo, los métodos tradicionales, como las transferencias bancarias internacionales a través de SWIFT o los pagos a través de intermediarios financieros, tienen limitaciones importantes que afectan a la competitividad de las empresas que se dedican a la importación, exportación o realización de transacciones transfronterizas.

Desafíos actuales en los pagos internacionales

Las empresas que envían dinero al extranjero se enfrentan a múltiples dificultades con los métodos de pago convencionales:

Altos costos operativos: Los pagos internacionales tradicionales son caros, con comisiones bancarias que oscilan entre 30 y 100 dólares por transferencia. Además de eso, los bancos aplican tipos de cambio desfavorables, inflando los costos sin transparencia. Muchas transacciones también pasan por bancos intermediarios, cada uno de los cuales añade comisiones y demoras, lo que hace que los pagos transfronterizos sean ineficientes y costosos.

Tiempos de liquidación lentos: Las transferencias bancarias internacionales pueden tardar de 2 a 5 días hábiles, lo que se ralentiza debido a las limitaciones del horario bancario, los fines de semana y las revisiones de cumplimiento. Los pagos también pueden retenerse o rechazarse debido a revisiones regulatorias, lo que provoca demoras que interrumpen el flujo de caja y las operaciones comerciales.

Intermediarios innecesarios: Las transacciones de SWIFT dependen de varios bancos corresponsales, cada uno de los cuales cobra comisiones y aumenta los tiempos de liquidación. Estos intermediarios añaden complejidad y riesgo, ya que cada paso adicional aumenta la posibilidad de errores, retrasos o bloqueos de los pagos.

Falta de transparencia y trazabilidad: Las empresas tienen una visibilidad limitada en tiempo real al realizar transferencias bancarias. Los pagos no se pueden rastrear al instante, lo que obliga a las empresas a confiar en las confirmaciones manuales de los destinatarios. Esta falta de transparencia complica la conciliación y retrasa la presentación de informes financieros.

Restricciones bancarias y de capital: En los mercados con controles cambiarios, las empresas suelen tener dificultades para enviar pagos internacionales. Algunos países bloquean las transferencias o imponen límites estrictos, lo que provoca retrasos y costes adicionales. Las empresas de estas regiones necesitan soluciones alternativas para mover los fondos de manera eficiente sin restricciones excesivas.

Stablecoins

¿Qué son?

Las stablecoins son activos digitales diseñados para mantener un valor estable, están diseñados para mantener un valor estable, respaldados 1:1 por una moneda fiduciaria (como el dólar estadounidense, el euro o el real brasileño) o una cesta de activos financieros. A diferencia de las criptomonedas como Bitcoin o Ethereum, que son muy volátiles, las stablecoins ofrecen precios más predecibles, lo que las hace aptas para pagos internacionales.

Vinculadas 1:1 a las monedas fiduciarias, combinan la estabilidad del dinero tradicional con la eficiencia y la transparencia de la tecnología blockchain.

Ventajas clave de usar stablecoins para pagos internacionales:

- Liquidación casi instantánea: Si bien una transferencia bancaria puede tardar días, una transacción de stablecoins se liquida en minutos o segundos.

- Costos de transacción más bajos: El envío de stablecoins a través de Tron (TRC-20) o Solana (SPL) cuesta menos de 1 dólar, en comparación con los 30 a 100 dólares de una transferencia SWIFT.

- Disponibilidad global las 24 horas del día: Los fondos se pueden enviar y recibir en cualquier momento, sin depender del horario bancario o los días festivos.

- Sin intermediarios: No hay necesidad de bancos corresponsales, lo que reduce la fricción y el riesgo de retención de fondos.

- Mayor transparencia y trazabilidad: Los pagos se pueden verificar en tiempo real mediante exploradores de cadenas de bloques.

Monedas estables para pagos internacionales

Existen diferentes tipos de monedas estables, pero las más relevantes para los pagos internacionales son stablecoins respaldadas por dinero fiduciario, que están respaldados por efectivo o equivalentes de efectivo.

Cuando una stablecoin afirma ser respaldado 1:1, significa que por cada unidad emitida (p. ej., 1 USDC o 1 USDT), hay un dólar estadounidense real o un activo equivalente mantenidos en las reservas de la sociedad emisora.

Ejemplo: Si hay 100 millones de USDC en circulación, Circle (el emisor) debe tener 100 millones de dólares estadounidenses o activos equivalentes de bajo riesgo en una cuenta bancaria o inversiones a corto plazo.

Esta estructura garantiza que, en cualquier momento, los usuarios puedan canjear sus monedas estables por dinero fiduciario, lo que reduce el riesgo de que la moneda pierda su paridad 1:1 con el dólar estadounidense.

¿Por qué las stablecoins son seguras dentro del sistema financiero?

Respaldado por activos líquidos y seguros: A diferencia de muchas criptomonedas que dependen exclusivamente de la oferta y la demanda del mercado, las stablecoins respaldadas por dinero fiduciario están respaldadas por activos financieros tradicionales, lo que garantiza que su valor se mantenga estable.

Ejemplos de reservas confiables:

Bonos del Tesoro de EE. UU. → Considerado uno de los activos financieros más seguros del mundo.

Depósitos bancarios en dólares estadounidenses → Mantenido en bancos regulados con protección de seguro.

Esto significa que, en una crisis financiera, los emisores pueden vender estos activos para garantizar el reembolso de los tokens en circulación, garantizando la liquidez y la estabilidad.

Sujeto a auditorías y supervisión reglamentaria (según el emisor): No todas las stablecoins tienen el mismo nivel de transparencia. Algunas, como el USDC, están sujetas a auditorías periódicas por parte de terceros para garantizar que las reservas sean reales y accesibles.

USDC (Círculo) → Publica auditorías mensuales verificadas por Grant Thornton, una de las principales firmas de contabilidad del mundo.

USDT (Tether) → Ha mejorado su transparencia, pero aún se enfrenta a un escrutinio con respecto a sus reservas y procesos de auditoría.

Conversión rápida a moneda fiduciaria: Una de las principales ventajas de las stablecoins es su convertibilidad inmediata a fiat a través de bolsas o plataformas OTC (de venta libre).

Esto significa que las empresas pueden recibir pagos en USDT o USDC y convertirlos en dólares, euros o reales brasileños en cuestión de minutos, sin esperar a los procesos bancarios tradicionales.

Las stablecoins más utilizadas para pagos internacionales: USDC y USDT

En el comercio internacional, las dos stablecoins más utilizadas para los pagos B2B son el USDC (USD Coin) y el USDT (Tether USD). Ambas están respaldadas por dólares estadounidenses y permiten transferencias rápidas y de bajo costo sin la necesidad de intermediarios bancarios.

Comparación entre USDC y USDT para pagos empresariales:

En la práctica, muchas empresas utilizan ambas stablecoins, según el tipo de transacción y las preferencias del proveedor.

Comparación entre las stablecoins y los métodos de pago tradicionales

Las empresas que gestionan pagos internacionales suelen utilizar métodos tradicionales, como las transferencias bancarias SWIFT o los pagos ACH. Sin embargo, estos sistemas conllevan costes elevados, plazos de liquidación prolongados y restricciones operativas, que pueden afectar al flujo de caja de una empresa.

Por el contrario, el uso de stablecoins para pagos internacionales ha reducido significativamente los tiempos de procesamiento, ha eliminado los intermediarios y ha proporcionado una solución más ágil y rentable.

Las stablecoins frente a las transferencias bancarias tradicionales

Casos de uso de stablecoins en empresas que envían pagos internacionales

Cuentas por pagar: Las empresas que realizan pagos recurrentes a proveedores internacionales pueden reducir los costos y los tiempos de liquidación mediante el uso de stablecoins en lugar de transferencias bancarias. Con el USDT o el USDC, los pagos se ejecutan en minutos y sin intermediarios, lo que garantiza una trazabilidad total y elimina las altas comisiones bancarias.

Optimización del flujo de caja global: Las stablecoins permiten a las empresas mover capital entre países sin depender de restricciones bancarias ni incurrir en costos de intermediación. Esto mejora la disponibilidad de liquidez en los principales mercados y facilita la distribución eficiente de los fondos entre las filiales que operan en múltiples jurisdicciones.

Pagos de nómina internacionales: Las empresas con empleados o contratistas en diferentes países pueden usar las stablecoins para pagar los salarios, eliminando las barreras bancarias y reduciendo los altos costos asociados con las transferencias internacionales.

Por ejemplo, un desarrollador de Europa o un profesional independiente de Argentina pueden recibir el pago en USDC y convertirlo a su moneda local sin perder valor debido a conversiones innecesarias.

Protección contra la devaluación: Las empresas que operan en economías con una inflación alta pueden proteger su capital convirtiendo los ingresos locales en stablecoins, evitando la depreciación de su moneda nacional.

Acceso a los mercados internacionales sin cuentas bancarias locales: Las empresas que buscan expandirse a nuevos mercados pueden usar stablecoins para pagos y cobros sin la necesidad de abrir cuentas bancarias locales en el extranjero.

Cómo realizar pagos internacionales con stablecoins

Las empresas que buscan realizar pagos con stablecoins tienen dos opciones principales: enviar fondos directamente a través de redes blockchain como Ethereum o Tron o utilizar plataformas fintech especializadas que optimicen el proceso.

El método apropiado depende de factores como el volumen de transacciones, la preferencia del destinatario y la necesidad de una conversión fiduciaria.

Pagos directos a través de redes blockchain

Las stablecoins como USDT y USDC operan en múltiples blockchains, lo que permite a las empresas enviar pagos internacionales descentralizado, sin intermediarios bancarios. Este método requiere que ambas partes tengan carteras compatibles y un conocimiento básico de cómo funcionan las redes blockchain:

1. Elegir la red adecuada

Cada blockchain tiene diferentes costos y velocidades de procesamiento, lo que afecta a la experiencia de pago:

Ethereum (ERC-20): Alta seguridad y adopción global, pero tarifas de transacción más altas.

Tron (TRC-20): Confirmaciones rápidas y de bajo costo, ideales para pagos comerciales frecuentes.

Solana (SPL): Transacciones casi instantáneas y rentables, aunque con una adopción menor.

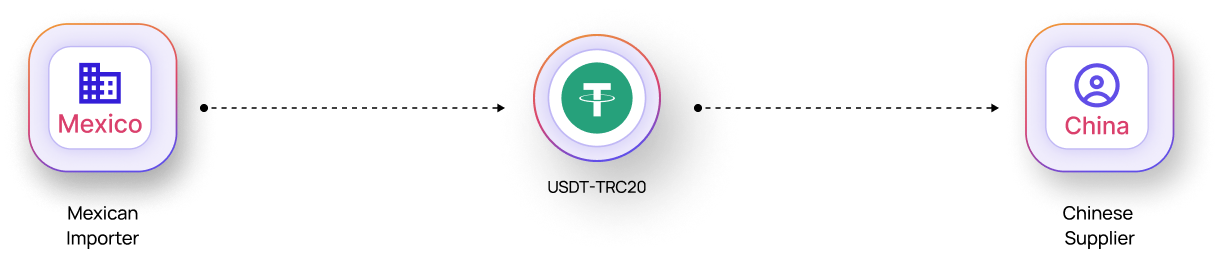

Ejemplo: Un importador mexicano puede pagar a un proveedor chino enviando USDT-TRC20 directamente desde su MetaMask o Trust Wallet, asegurándose de que el destinatario tenga una billetera compatible en la misma red.

2. Compra y depósito de stablecoins

Si la empresa aún no tiene stablecoins en su billetera, se pueden comprar en plataformas como Kraken. Una vez adquiridos, los fondos deben transferirse a la billetera que se utilizará para el pago.

3. Enviar el pago y verificar la transacción

Desde la billetera, se ingresa la dirección del destinatario, se selecciona el monto y se paga la tarifa de red. La transacción se confirma en cuestión de minutos y se puede verificar en exploradores de blockchain como Etherscan (Ethereum) o Tronscan (Tron).

Pagos con stablecoins a través de plataformas de tecnología financiera

Para las empresas que requieren una forma más fluida de gestionar los pagos internacionales con stablecoins,, las plataformas fintech especializadas ofrecen una solución que elimina la complejidad técnica de operar directamente en redes de cadenas de bloques.

Estas plataformas integran stablecoins en un sistema de pago corporativo, lo que permite a las empresas procesar transacciones sin interactuar manualmente con las redes blockchain.

Las principales ventajas de utilizar una tecnología financiera para los pagos con stablecoins incluyen:

- Conversión flexible entre monedas locales y monedas estables.

- Reducción de los errores de transacción al validar automáticamente las direcciones de los monederos y

redes blockchain. - Integración con cuentas corporativas para mejorar la trazabilidad y el cumplimiento de las normativas.

Cómo realizar pagos y liquidaciones internacionales con stablecoins a través de Conduit

Conduit permite a las empresas usar stablecoins para agilizar los pagos a los proveedores, administrar la tesorería en USD y convertir fondos de manera eficiente entre monedas locales y stablecoins.

Para empezar, las empresas deben abrir una cuenta en Conduit, que les permite gestionar los pagos tanto en monedas fiduciarias como en stablecoins. Una vez registrado, iniciar un pago es sencillo. La empresa selecciona la moneda de origen y destino, eligiendo entre opciones fiduciarias como BRL, COP o USD y stablecoins como USDC (ETH), USDT (ETH) o USDT (TRX). La aplicación web proporciona cotizaciones en tiempo real, lo que garantiza una total transparencia en las tasas de conversión.

Por qué las empresas eligen Conduit

- Envía pagos a proveedores internacionales en USD con stablecoins.

- Pague a los empleados remotos en stablecoins en regiones con monedas volátiles.

- Convierte fondos locales (BRL, MXN, COP) en stablecoins para liquidar los pagos internacionales más rápido.

- Utilice stablecoins para la gestión de la tesorería corporativa y protéjase contra la volatilidad de las divisas.

Esto flujo de pagos permite a las empresas beneficiarse de la velocidad y la eficiencia de las transacciones de stablecoins sin riesgos adicionales ni complejidades operativas. Conduit simplifica la conversión de divisas e integra stablecoins en los pagos globales de forma segura y eficiente.

Conceptos erróneos y desafíos comunes del uso de stablecoins

Si bien las stablecoins respaldadas por dinero fiduciario, como el USDC y el USDT, tienen claras ventajas para las empresas de comercio electrónico, existen conceptos erróneos y desafíos que deben aclararse. Comprenderlas puede ayudar a las empresas a adoptar las stablecoins con confianza y a sortear los posibles obstáculos de manera eficaz.

Conceptos erróneos comunes

¿Las stablecoins son tan riesgosas como otras criptomonedas?

Muchas personas asocian las stablecoins con la volatilidad de las criptomonedas como Bitcoin o Ethereum. Sin embargo, las stablecoins respaldadas por dinero fiduciario son diferentes. Stablecoins están diseñados para mantener un valor constante porque están vinculados a monedas fiduciarias como el dólar estadounidense. Por ejemplo, siempre se pretende que 1 USDC valga 1 dólar.

Ejemplo: Si recibes 500$ en USDC hoy, su valor se mantiene estable, a diferencia de Bitcoin, que podría fluctuar un 10% o más en un solo día.

Si bien la tecnología blockchain detrás de las stablecoins se comparte con otras criptomonedas, su estabilidad y el respaldo de activos reales las hacen más confiables para los pagos de comercio electrónico.

¿Las stablecoins requieren experiencia técnica para su uso?

Algunas empresas dudan en adoptar stablecoins por temor a necesitar habilidades técnicas avanzadas o conocimientos de blockchain. El uso de las stablecoins es sencillo, gracias a las carteras y plataformas de pago fáciles de usar. Muchas soluciones son tan fáciles de usar como las aplicaciones bancarias tradicionales.

Ejemplo: Plataformas como Trust Wallet o Coinbase permiten a los usuarios enviar y recibir USDC o USDT con solo unos pocos clics, de forma similar a enviar una transferencia bancaria.

Además, muchos procesadores de pagos ahora integran stablecoins, lo que permite a las empresas aceptar pagos sin problemas sin necesidad de comprender en profundidad la tecnología blockchain.

Desafíos clave

Incertidumbre regulatoria en algunos países

Las stablecoins existen en una zona gris regulatoria en muchas regiones, y las leyes aún están evolucionando. Algunos gobiernos son cautelosos con respecto a los activos digitales y pueden imponer restricciones a su uso para transacciones comerciales. Esta incertidumbre afecta a las empresas, especialmente a las de comercio electrónico, que deben mantenerse informados sobre la situación legal de las stablecoins en su país para garantizar su cumplimiento. Para gestionar esto, las empresas deben trabajar con proveedores de pago confiables que siguen las normas locales. Mantenerse al día con las actualizaciones legales y consultar a los expertos cuando sea necesario también puede ayudarlos a evitar posibles problemas.

Adopción limitada por parte de las instituciones financieras tradicionales

A pesar de la creciente adopción, muchos bancos e instituciones financieras aún tienen que integrar completamente las stablecoins en sus sistemas. Esto puede dificultar que las empresas conviertan las stablecoins en monedas fiduciarias o las integren con los servicios bancarios tradicionales. Para solucionar este problema, las empresas pueden asociarse con procesadores de pagos que admiten transacciones de stablecoins a monedas fiduciarias. Usando cuentas multidivisa que aceptan stablecoins también pueden simplificar las operaciones financieras y mejorar la gestión del flujo de caja.

El futuro de los pagos con stablecoins

Las stablecoins han pasado de ser un activo criptográfico de nicho a convertirse en una solución clave para los pagos comerciales internacionales. Con la expansión del comercio digital y la demanda de métodos de pago más rápidos y eficientes, la adopción seguirá creciendo, especialmente entre los importadores, los exportadores, las empresas de tecnología financiera y las empresas que operan a nivel mundial.

Un factor clave de esta evolución es el impulso regulatorio en los principales mercados financieros. Las stablecoins están ganando una aceptación cada vez mayor en el sistema financiero tradicional, y una normativa más clara facilitará su integración con los bancos y las empresas de tecnología financiera, reforzando su uso para los pagos entre empresas y las transacciones internacionales.

Además, las grandes instituciones financieras están estudiando la posibilidad de emitir sus propias stablecoins e integrar estos activos en su infraestructura de pagos. A medida que más empresas de tecnología financiera y bancos comiencen a ofrecer stablecoins dentro de marcos regulados, su uso en los pagos internacionales se generalizará aún más, lo que permitirá a las empresas transferir fondos de forma instantánea, con costes más bajos y sin intermediarios innecesarios.

Accede al movimiento de dinero respaldado por stablecoins en la plataforma de pagos de Conduit

Descubra cómo Conduit puede ayudar a su empresa a superar los problemas que supone realizar y recibir pagos internacionales con stablecoins.

Con Conduit puedes:

- Ingresar en cuentas bancarias de todo el mundo. Utiliza métodos de pago locales para enviar pagos globales directamente a cuentas bancarias en EE. UU., China, América Latina, África y más allá.

- Acceder a tasas competitivas en múltiples monedas. Nuestro flujo de fondos personalizado está diseñado para reducir las comisiones y mejorar la velocidad de las conversiones fiduciarias locales.

- Utilice una aplicación web fácil de usar. Nuestra sencilla aplicación web hace que las operaciones de pago sean más rápidas, fáciles y económicas para tu equipo.

Para obtener más información, visita conduitpay.com o contacta con nosotros directamente y descubre cómo podemos ayudar a tu negocio.