Crypto Regulation News in Africa: An overview of virtual asset and stablecoin frameworks

Explore the latest crypto regulation developments in Africa and understand how virtual asset and stablecoin frameworks are taking shape.

Conduit

January 8, 2026

In recent years, Africa’s financial architecture has entered a period of structural transition. The continent is moving away from a historically cautious stance toward financial innovation and an accelerated implementation of new digital infrastructures and regulatory models, which are already impacting the daily lives of individuals and businesses across the region.

African consumers have shown strong appetite for adopting new financial technologies. The continent leads the world in mobile digital payments adoption, accounting for more than 60% of global usage. According to recent data from Business Insider, approximately 43.5 million people in Africa owned cryptocurrencies in 2024, an increase of about 8.5% compared to the previous year, with countries such as South Africa, Nigeria, Kenya, Egypt, and Tanzania among the region’s leading markets.

Sub-Saharan Africa has emerged as one of the world’s most active crypto markets in terms of real-world usage, with particular emphasis on the use of stablecoins for payments and transfers beyond purely speculative activity.

Stablecoins accounted for a significant share of crypto transactions in the region, driving use cases related to cross-border payments and treasury management, while helping mitigate the effects of currency volatility and limited access to U.S. dollars.

Currency volatility remains a major challenge across the continent, and the use of stablecoins has played an important role in protecting purchasing power and commercial margins. Ethiopia, for example, experienced approximately 30% currency depreciation in 2024, followed by an estimated 180% increase in stablecoin usage over the same period.

This growth has also been strongly driven by recent regulatory advancements across several African countries, which have introduced clearer and more consistent legal frameworks. These developments have increased confidence among individuals and businesses to use digital assets for real-world applications and legitimate financial operations.

Regulatory Momentum in Africa’s Crypto Market

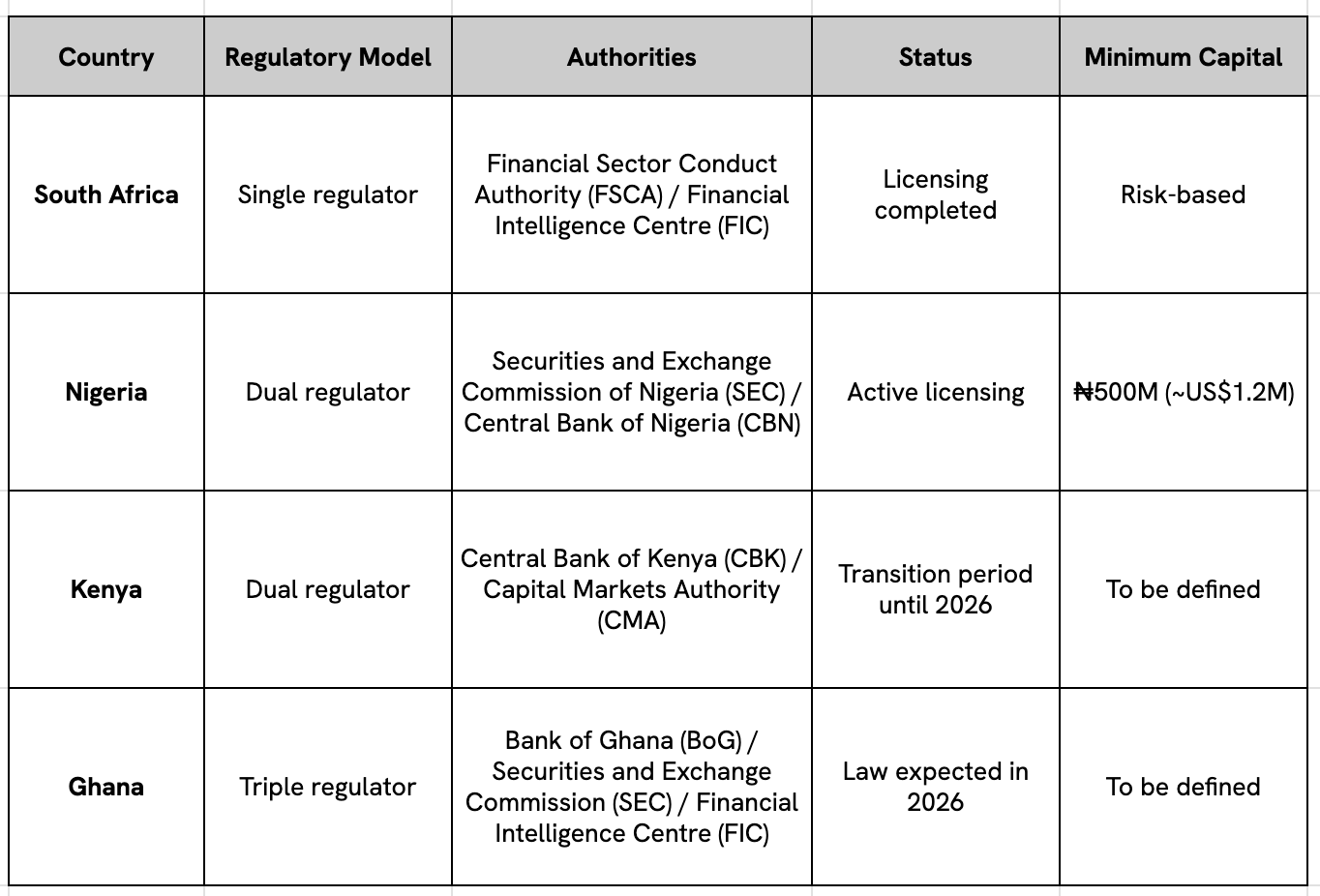

Between 2022 and 2025, four of Africa’s most influential economies in digital assets, South Africa, Nigeria, Kenya, and Ghana, began to lead this shift by adopting distinct yet clearly convergent regulatory models. Their shared objective is to capture the economic potential of blockchain technology and stablecoins while reducing systemic risks and structural vulnerabilities.

Africa’s new regulatory narrative is increasingly defined by key pillars such as formal licensing regimes, capital requirements, strong governance standards, robust KYC processes, and the implementation of the Travel Rule, a FATF recommendation that requires the verification and transmission of transaction-related information between regulated entities.

The official removal of South Africa and Nigeria from the FATF grey list in October 2025 further symbolizes this turning point and sends a clear signal to global markets that the continent has made significant progress and entered a new phase of regulatory maturity.

See below the key developments across the region and a summary of the current status of Virtual Asset Service Provider (VASP) regulation in some African economies.

Crypto Regulation News in South Africa: A Model of Regulatory Integration

South Africa has built the most mature and integrated regulatory environment for virtual assets on the African continent. Rather than creating standalone crypto legislation, the country chose to incorporate cryptoassets into its existing legal and regulatory framework.

In October 2022, the Financial Sector Conduct Authority (FSCA) classified cryptoassets as “financial products,” bringing Virtual Asset Service Providers (VASPs) under the scope of the FAIS Act. This move imposed higher standards of conduct, governance, and professional fitness on market participants.

The FAIS Act (Financial Advisory and Intermediary Services Act, No. 37 of 2002) is South Africa’s primary legislation governing the provision of financial advisory and intermediary services.

The licensing process, which began in June 2023, resulted in hundreds of applications and dozens of institutions already licensed, helping to consolidate a more professionalized market. In parallel, South Africa advanced rapidly on AML compliance with the implementation of the Travel Rule through Directive 9 issued by the Financial Intelligence Centre (FIC), requiring the collection, verification, and transmission of sender and beneficiary data for crypto transfers.

The outcome is a more transparent ecosystem, aligned with global standards and increasingly attractive to institutional capital.

Crypto Regulation News in Nigeria: From Prohibition to Institutionalization

Nigeria perhaps represents the most dramatic regulatory shift in the region. After imposing a banking ban on the crypto sector in 2021, which pushed activity into the peer-to-peer (P2P) market, the country has fully reversed its approach.

Starting in 2023, the Central Bank of Nigeria resumed allowing banking operations for licensed Virtual Asset Service Providers (VASPs), and the Investments and Securities Act of 2025 (ISA 2025) formally recognized digital assets as securities when they qualify as investment instruments.

Nigeria has adopted a clearly institutional approach, introducing some of the highest capital requirements for VASPs globally (approximately US$1.2 million), along with strict rules on fund segregation, financial guarantees, and tax oversight. The objective is to enable financial innovation while ensuring it is driven only by well-capitalized and tightly supervised operators.

Crypto Regulation News in Kenya: High Expectations for Interoperability with M-Pesa

Kenya consolidated its regulatory shift with the enactment of the Virtual Asset Service Providers (VASP) Act of 2025, signed by President William Ruto in October 2025 and in force since November 4, 2025. The new law marks a clear departure from years of informal guidance in favor of a formal and comprehensive legal framework.

The country adopted a dual-regulator model, with the Central Bank of Kenya overseeing payments and stablecoins, while the Capital Markets Authority regulates trading and investment platforms.

The legislation introduces robust requirements around governance, asset segregation, audits, and local presence, along with a transition period extending into 2026. On the tax front, Kenya refined its approach by replacing a tax on the gross value of transactions with a consumption tax on platform fees, reducing economic distortions and operational friction.

With high mobile money penetration through platforms such as M-Pesa, Kenya positions itself as one of the strongest candidates to efficiently and compliantly integrate stablecoins, local payment rails, and regional remittances.

Crypto Regulation News in Ghana: Gradual Implementation with a Focus on Payments

Ghana is taking a more gradual yet strategic approach. The country is finalizing its VASP Bill, with full licensing expected to begin in 2026, and has established the Virtual Assets Regulatory Office (VARO) within the Central Bank.

The purpose of VARO is to centralize the supervision and regulation of virtual assets in Ghana, ensuring that VASPs operate in line with global AML/CFT standards.

Ghana’s key differentiator lies in the integration of payments, stablecoins, and the modernization of international trade, as demonstrated by initiatives such as Project DESFT (Digital Economy Semi-Fungible Token). This pilot combined a central bank digital currency (CBDC) with stablecoins in real financial transactions. The model prioritizes controlled innovation, regulatory sandbox testing, and AML/CFT alignment from the outset.

Summary: From Informal Adoption to Institutional Integration

Africa’s leading economies have reached an irreversible point of institutionalization of virtual assets, with strong potential for expansion across the continent. What began as a peer-to-peer phenomenon to solve banking limitations is now being integrated into the formal financial architecture.

The message is clear: the continent is open to innovation, but within clear rules, active supervision, and global compliance standards.

Stablecoins and blockchain are no longer marginal technologies. They are becoming structural components, especially in cross-border payments, remittances, FX protection, and integration with local payment rails.

Regulatory Comparison Across Key African Markets

Discover Conduit’s Stablecoin Infrastructure and Take Your Operations to the Next Regulatory Level in Africa

Integrate stablecoins into your financial operations with an infrastructure built to meet the highest global regulatory standards. Conduit connects digital assets to local financial rails, enabling companies, banks, and fintechs to operate cross-border payments, treasury management, and international settlements across Africa with full compliance, transparency, and predictability.

If your strategy requires scale, regulatory certainty, and operational efficiency, Conduit is the partner that turns regulation into a competitive advantage.

.jpg)

.jpeg)