Virtual IBAN: What it is and the benefits for cross-border payments

Learn how Virtual IBANs streamline cross-border payments in EUR and GBP with faster settlement and local-like efficiency.

Conduit

December 30, 2025

Sending and receiving international payments is still a friction-heavy process for many businesses. While domestic payments have evolved exponentially worldwide, individuals and companies continue to face bureaucracy, delays, and high costs in cross-border transactions. In this context, seeking alternatives that make payment experiences increasingly local proves highly advantageous.

Virtual IBANs play a key role in transactions involving GBP and EUR, bringing the international payment experience closer to that of domestic payments. With a Virtual IBAN, fintechs and businesses around the world can rely on a dedicated banking identifier, enabling faster international collections, simplified reconciliation, and the ease of a local transaction.

As companies grow and begin working with multiple clients and currencies across different countries, collection complexity increases, and lack of visibility directly impacts cash control and financial predictability.

In this article, we will explore:

- What is an IBAN number

- How a Virtual IBAN works

- The difference between a Virtual IBAN and a SWIFT code

- The benefits of Virtual IBAN for businesses

What is an IBAN number?

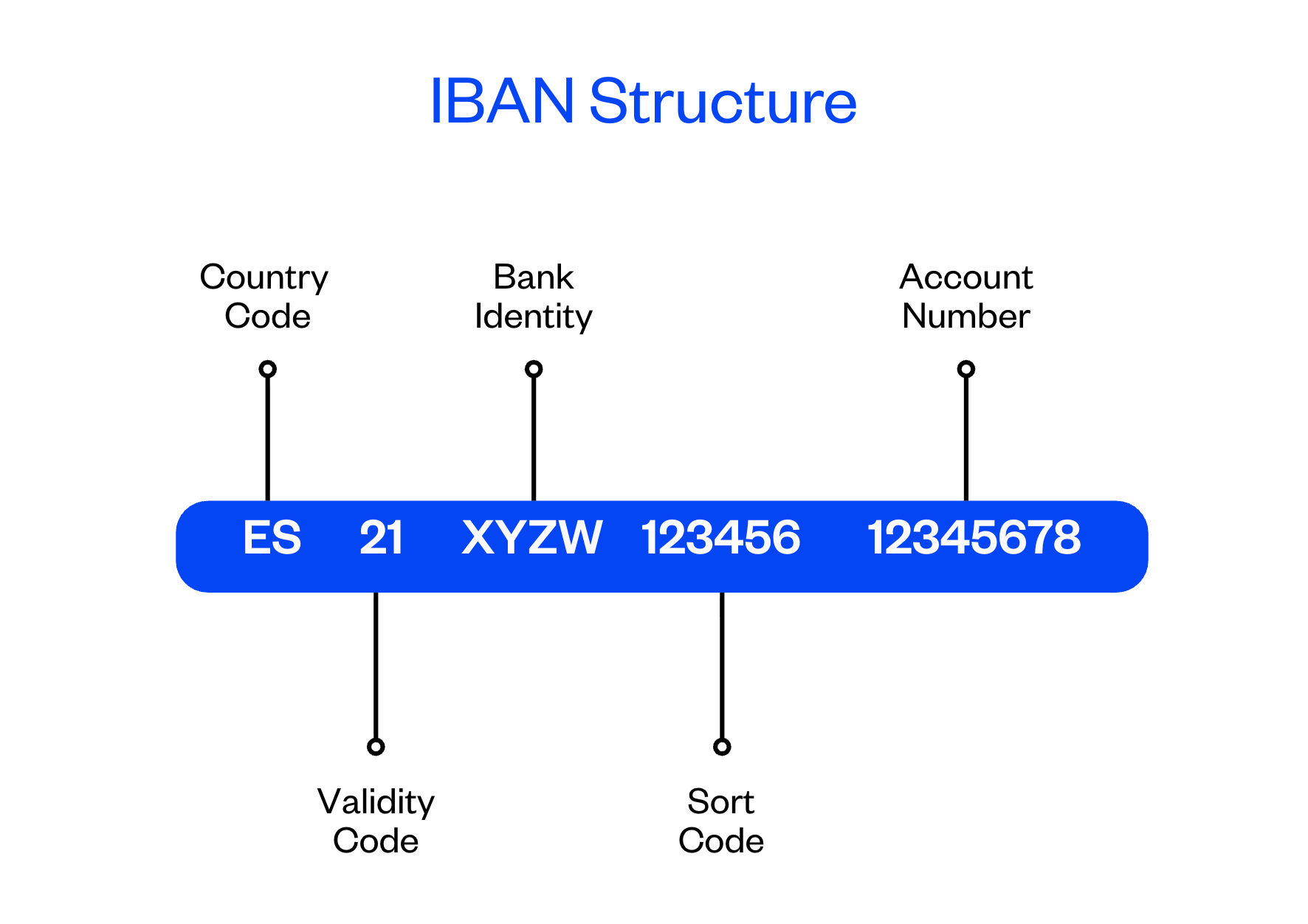

An IBAN (International Bank Account Number) functions as a bank account identifier and is primarily used in European countries and the United Kingdom to facilitate international bank transfers.

The IBAN format is a continuous alphanumeric code of up to 34 characters, starting with a two-letter country code followed by two check digits. Below is an example of an IBAN structure:

How a Virtual IBAN works

A Virtual IBAN (vIBAN) is a unique banking identifier that can be issued in the name of a company to receive payments directly, without the need to open or maintain a traditional bank account linked to that number. Simply put, it functions as a collection address, allowing funds to be routed to an existing company account.

The key differentiator is that each Virtual IBAN is unique, enabling businesses to associate different IBANs with specific clients, projects, or currencies. This makes it much easier to identify who made each payment and to automate financial reconciliation processes without errors or delays.

Difference Between a Virtual IBAN and a SWIFT Code

A SWIFT code identifies a financial institution within a global messaging network. It is used to exchange payment instructions between banks, but it does not identify a specific account nor guarantee direct settlement. Payments routed via SWIFT typically rely on correspondent banks, pass through multiple intermediaries, and are subject to longer settlement times, higher costs, and limited predictability. SWIFT is essentially a communication layer between institutions, not a payment rail itself.

A Virtual IBAN, on the other hand, directly identifies an account, even if in a logical form and not necessarily tied to a traditional physical bank account. It provides direct access to local payment infrastructures, such as SEPA for EUR and equivalent schemes for GBP, allowing international transfers to be processed as domestic payments.

While SWIFT connects banks globally, a Virtual IBAN connects the end user directly to local payment infrastructure in a much simpler way.

Benefits of Virtual IBAN for Businesses

A Virtual IBAN enables the receipt of international payments while delivering a truly local payment experience.

With a Virtual IBAN, businesses gain:

- Expanded global reach with a local experience in EUR and GBP.

- Lower costs by eliminating intermediaries and correspondent banks.

- Greater clarity on who paid what, improving audit and reconciliation processes.

- Faster transaction processing.

With Virtual IBANs, companies operating across regions such as Latin America, Africa, Asia, and other parts of the world can receive payments in GBP and EUR with the same simplicity and speed as a business based in Europe or the United Kingdom. And best of all, this is achieved without the need to establish a local legal entity, while remaining fully compliant with regulatory requirements.

The day-to-day result is greater efficiency and liquidity, supported by a much more scalable financial operation, which is especially critical for B2B platforms, marketplaces, fintechs, and businesses with high volumes of receivables.

Start using Virtual IBANs with Conduit

Conduit’s Virtual IBAN functionality reinforces our commitment to removing the barriers of the traditional financial system by simplifying processes and enabling global capital to flow more freely.

Combined with our stablecoin infrastructure, it connects local banking rails with natively digital layers, enabling faster, more predictable, and more efficient international payments.

The solution is ideal for businesses operating at scale, delivering greater clarity, control, and agility in cross-border payments. Talk to our team and discover how Conduit can transform your global financial operations.

.jpg)

.jpeg)