What is IOF: Understanding Brazil’s Financial Operations Tax

Learn what IOF is, how it impacts financial transactions in Brazil, and its role in regulation and taxation.

Conduit

November 28, 2025

IOF (Imposto sobre Operações Financeiras, or Tax on Financial Operations in English) has been a frequent topic of discussion in recent months, largely due to changes introduced by the Brazilian federal government that impact both individuals and businesses. It is a subject of national and international relevance, as it also affects global companies operating in Brazil.

IOF is a tax applied to various financial transactions carried out in Brazil, such as credit operations, foreign exchange, insurance, investments and securities, with rates that vary according to the type of transaction. Understanding IOF is essential for accurate financial planning, as well as for gaining clarity about this important element of Brazil’s financial ecosystem.

In this article, we will explore:

- What is IOF and how it works

- Where IOF is charged in daily activities

- IOF 2025: how it stands after the changes

- Tips for reducing the effects of IOF on your business

- IOF on stablecoin payments

- Frequently Asked Questions about IOF - FAQs

What is IOF and how it works

IOF is an instrument of the Brazilian tax system that originated in 1966, and it was initially applied only to credit and insurance operations. After the 1988 Constitution, its scope was expanded to also include foreign exchange transactions and operations involving securities and financial assets.

Unlike most taxes, IOF has a unique characteristic: its rates can be modified by presidential decree and take effect immediately. This flexibility makes it a key tool for rapid adjustments in economic policy, especially for controlling inflation.

In addition to its revenue-raising role, the tax also allows the government to monitor the volume and profile of financial movements, such as credit, international transactions, and other operations.

Where IOF is charged in daily activities

In daily financial operations, IOF appears in multiple types of transactions. Below are the main categories in which this tax is applied.

Credit and Loans

- Loans and financing granted by banks or financial institutions.

- Domestic credit cards: credit usage and installment plans.

- International credit cards: purchases abroad or in a different currency, cash withdrawals outside Brazil, or installment payments in a foreign currency.

Foreign Exchange and International Transfers

- Purchase of foreign currency in cash.

- International transfers (sending money to other countries).

- Purchase of prepaid cards in foreign currency and the use of debit cards in a different currency.

Note: IOF varies depending on whether the transaction involves commercial exchange rates (for imports and exports) or financial exchange rates (transfers, investments, or tourism).

Investments

- Fixed-income and securities transactions (CDB, LC, investment funds subject to regressive IOF).

- Redemptions within a short period (less than 30 days) are subject to a daily regressive rate.

Insurance

Insurance premiums, such as life insurance or car insurance.

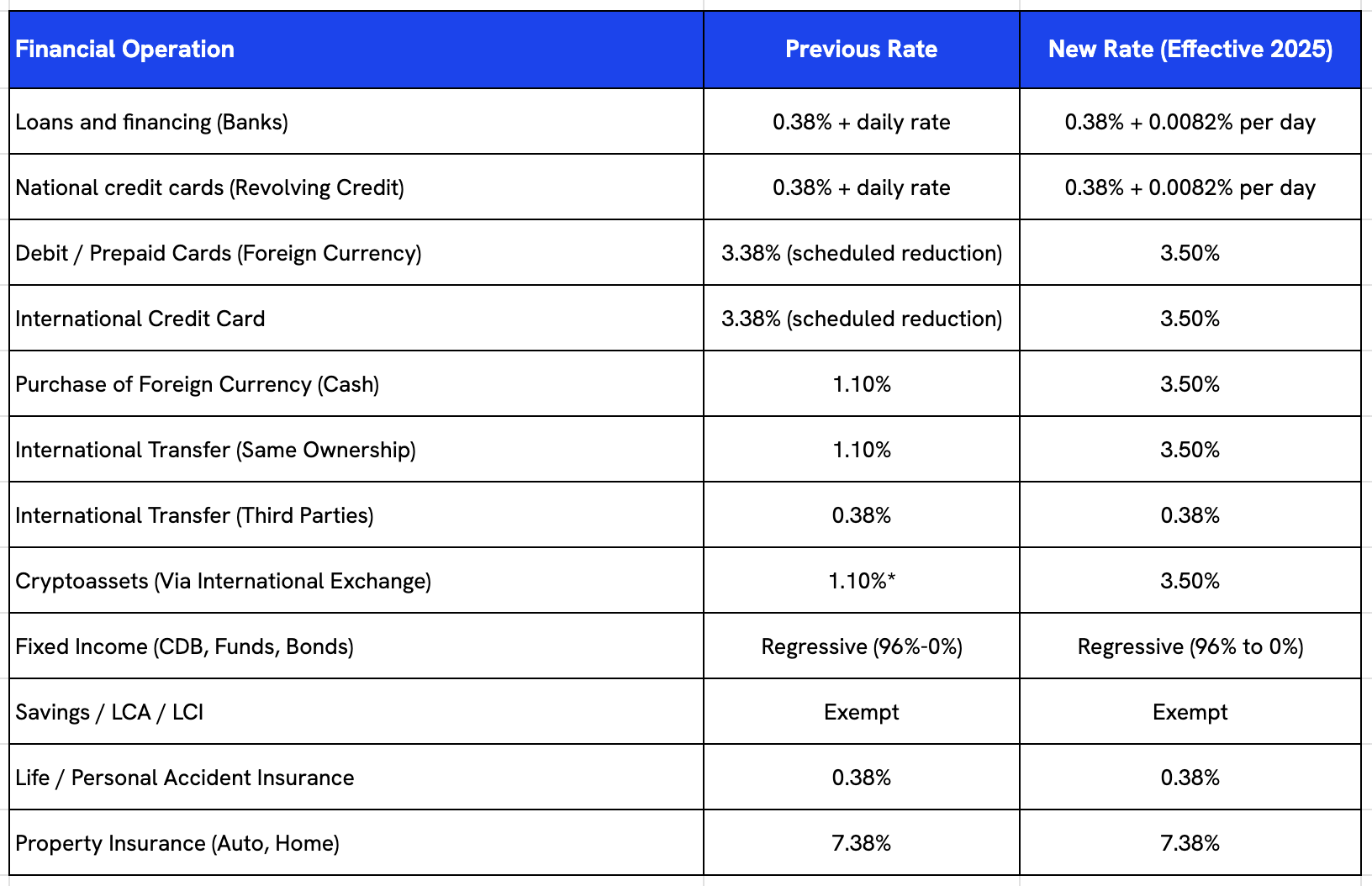

IOF 2025: how it stands after the changes

In 2025, IOF remained at the center of attention in the media and the corporate environment following the changes announced by the government in May, which were initially revoked and later implemented with some adjustments in July. With so many back-and-forth decisions, many questions arose regarding the current rates applied to operations subject to IOF.

Below are the rates in effect after the changes:

The Brazilian government maintained a strict separation between what is considered Foreign Trade (imports and exports) and what is considered Financial Movements (money and services).

While the IOF for international remittances between accounts belonging to the same company increased to 3.5 percent, the IOF for companies that import and export remained at zero in most cases, in order to avoid generating internal inflation.

Some tips for reducing the effects of IOF on your business

IOF rates directly impact the financial planning of both individuals and companies, and some of the recent changes represent significant differences that can affect cash flow.

We are seeing a scenario in which financing and receivables advances have become more expensive, and international purchases and investments have also been affected. Therefore, it is important to understand some practical strategies to mitigate the effects of IOF on your business’s liquidity.

Global treasury management

Managing accounts and receivables directly in foreign currency is a crucial strategy to avoid unnecessary conversion costs and triggering taxable events. By keeping funds in the original currency, the company creates a natural hedge and uses these resources for future international obligations without converting them back to the local currency.

💡 Conduit’s virtual account solutions are essential for this approach, providing a robust infrastructure for global treasury management that allows companies to hold, manage and allocate multi-currency balances efficiently, thereby avoiding repeated foreign exchange and tax exposure.

Payment strategy

When purchasing corporate products and services, it is essential to choose payment methods with lower IOF incidence. For example, opting to pay via international invoice (transfer) related to a service import contract instead of using a corporate credit card can drastically reduce the tax burden from 3.5 percent to 0.38 percent, or even 0 percent in specific cases.

💡 Conduit’s payment platform is designed specifically to streamline accounts payable processing. In addition to reducing IOF exposure by enabling efficient invoice payments, the platform also significantly reduces transactional costs and optimizes margins, ensuring that cross-border payments are as cost-effective as possible.

Volatility control

In a scenario where tax rates and exchange rates fluctuate, controlling volatility is essential for financial stability. Companies should adopt proactive hedging mechanisms to lock in costs and protect profit margins against sudden currency devaluations or regulatory tax adjustments.

This involves carefully monitoring foreign exchange exposure and the timing of remittances to ensure the business is not caught off guard by unfavorable market conditions that can further increase tax costs such as IOF.

Investments

For companies with liquidity in Brazil, paying attention to the IOF regressive table on fixed-income investments is essential. Because the tax applies heavily to short-term redemptions (decreasing from 96 percent to 0 percent over 30 days), efficient cash-flow planning should prioritize keeping assets for at least 30 days to obtain full tax exemption on returns.

For international investments, ensuring that remittances are correctly classified can also help avoid paying higher rates.

IOF on stablecoin payments

The digital asset market is undergoing a period of transformation with the implementation of new resolutions from the Central Bank of Brazil aimed at Virtual Asset Service Providers (VASPs), launched in November of this year.

It is important to understand that, at this initial stage, these guidelines are strictly regulatory and compliance-focused, aimed at preventing money laundering and identifying the parties involved in transactions. The current objective is to provide the regulator with visibility over capital flows and ensure that providers operate with governance standards similar to those of traditional financial institutions, without immediately changing the tax structure for the purchase of the asset itself.

Currently, IOF is not applied to international transactions conducted via stablecoin infrastructure. However, it is not ruled out that these regulations may soon be expanded to cover taxation, with IOF applied to the settlement of payments with stablecoins, aligning them with traditional foreign exchange operations.

Take your payments to the next level with Conduit’s stablecoin infrastructure

Conduit provides a complete infrastructure for your company to integrate stablecoin payments with full compliance, security, and efficiency. Connect today to more efficient financial flows, reduce transactional costs, and transform your payment and treasury management into a competitive advantage. Talk to our specialists and discover how to operate without borders while optimizing margins.

Frequently Asked Questions about IOF - FAQs

What is IOF?

IOF is the Tax on Financial Operations, a Brazilian tax applied to credit, foreign exchange, insurance, investments, and securities transactions.

What is the purpose of IOF?

In addition to generating revenue, it serves as a regulatory tool for the economy, such as inflation control, and allows the government to monitor the volume and profile of financial transactions in the country.

How can the effects of IOF be reduced?

By adopting strategies such as managing global treasury in different currencies, replacing corporate credit card usage with payments via invoices, implementing hedging to control volatility, and respecting the 30-day holding period for fixed-income investment redemptions.

Does IOF apply to payments with stablecoins?

Currently, it does not, as the recent regulations are strictly regulatory and not tax-related. However, it is expected that IOF may soon be applied to align these transactions with the tax costs of traditional foreign exchange operations.

.jpg)

.jpeg)