SEPA, Fedwire, Pix, M-Pesa, etc: How stablecoins bridge isolated rails for cross-border flows

Domestic rails are fast but isolated. Learn how stablecoins bridge networks worldwide and enable true cross-border interoperability.

Conduit

December 16, 2025

The local payment rails such as SEPA, Fedwire, FPS, SPEI, M-Pesa, Pix, and others, are the backbone of modern financial ecosystems. Every day, they support billions of domestic transactions with remarkable speed and efficiency.

In their respective regions, these systems have transformed how individuals and businesses move money locally by enabling real-time settlement, high availability and low operational friction. Their impact on financial inclusion, digitalization and economic activity is undeniable, making them some of the most advanced and trusted payment infrastructures in the world.

However, when it comes to cross-border transactions, the landscape looks very different, far less efficient and with limited interoperability with payment rails outside their own regions.

The lack of interoperability is not a flaw, but rather a consequence of the original design of these systems. They were originally designed to operate as closed domestic systems limited to the region’s own currency, not as global payment bridges. For international transfers, these rails still rely on legacy networks such as SWIFT.

Why they lack interoperability in global payments

These systems follow strict rules, and there are barriers of various kinds that prevent seamless integration with other payment networks. Among the main reasons are:

Legal barrier: Local payment rails operate under regulations that are only legally enforceable within their own jurisdictions. Their governing bodies have no authority to impose execution times, refund conditions, or fee structures on banks in other countries or regions.

Currency and technological barrier: Domestic payment systems are designed to settle exclusively in their local currency. They do not include native foreign exchange (FX) conversion mechanisms within their core settlement layers.

Network disconnection: There is no direct “pipe” connecting one country’s clearing system to another. A domestic rail cannot natively route payments to a foreign clearing network.

Data standardization: Although the world is moving toward ISO 20022, global adoption remains fragmented. How a domestic participant structures payment data may not be fully compatible with institutions operating outside that scheme.

In summary, A2A systems require bilateral or multilateral connections between national infrastructures and national scheme rules. Building these links traditionally demanded significant institutional coordination, standardized data flows, aligned authorization protocols, and regulatory trust - until the emergence of stablecoins.

Stablecoin: The solution for greater interoperability in cross-border payments

The technology behind stablecoins has emerged not as a replacement but as the “pipe” that has long been missing – the layer that can connect payment networks that historically operate in isolation, such as Fedwire, SEPA, M-Pesa, Pix, ACH, CHAPS, and FPS.

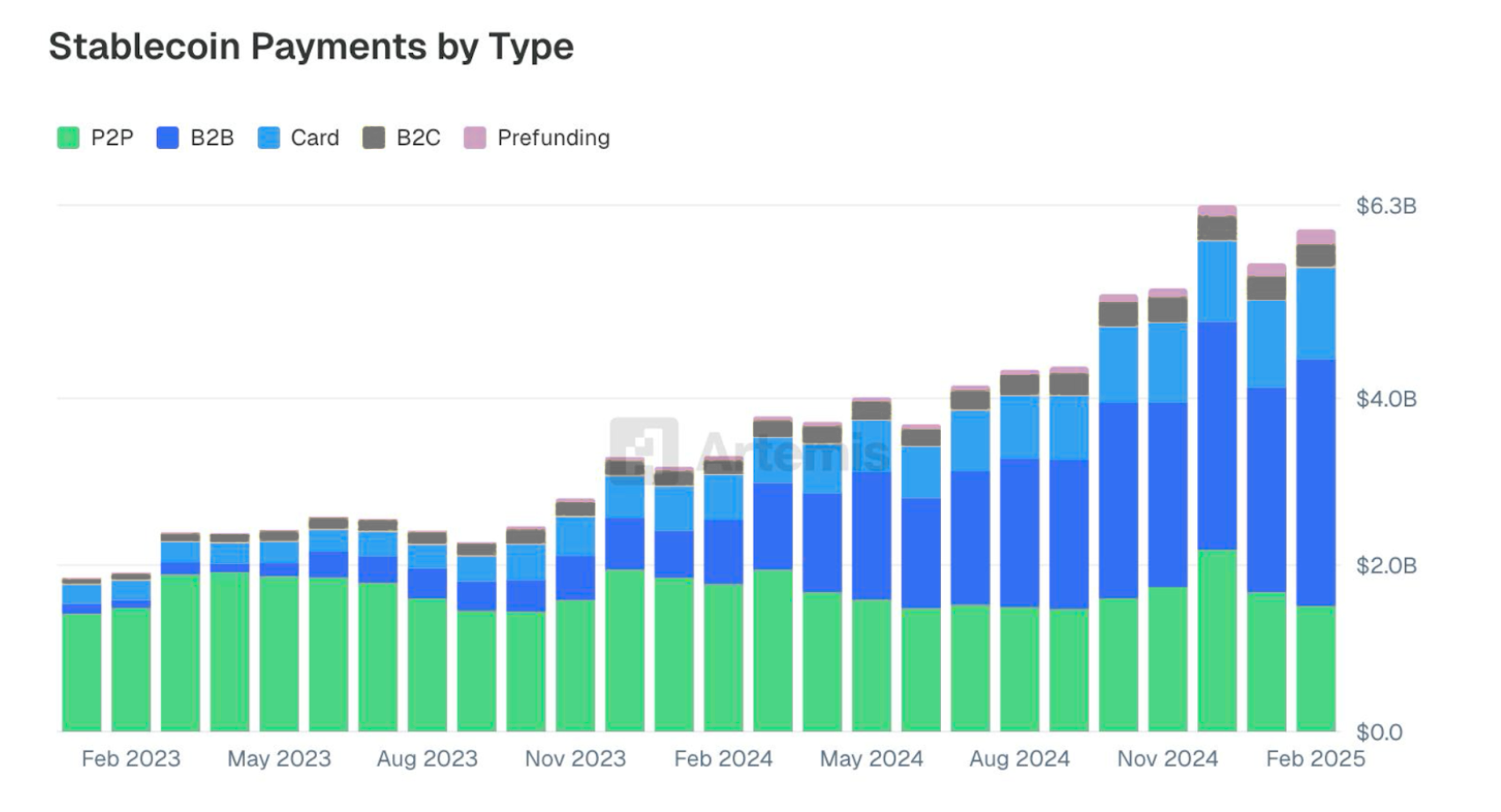

The stablecoin market has been growing rapidly, surpassing US$300 billion in total market capitalization in 2025. B2B payments already represent the majority of these flows, with transaction volumes increasing 50-fold since 2023.

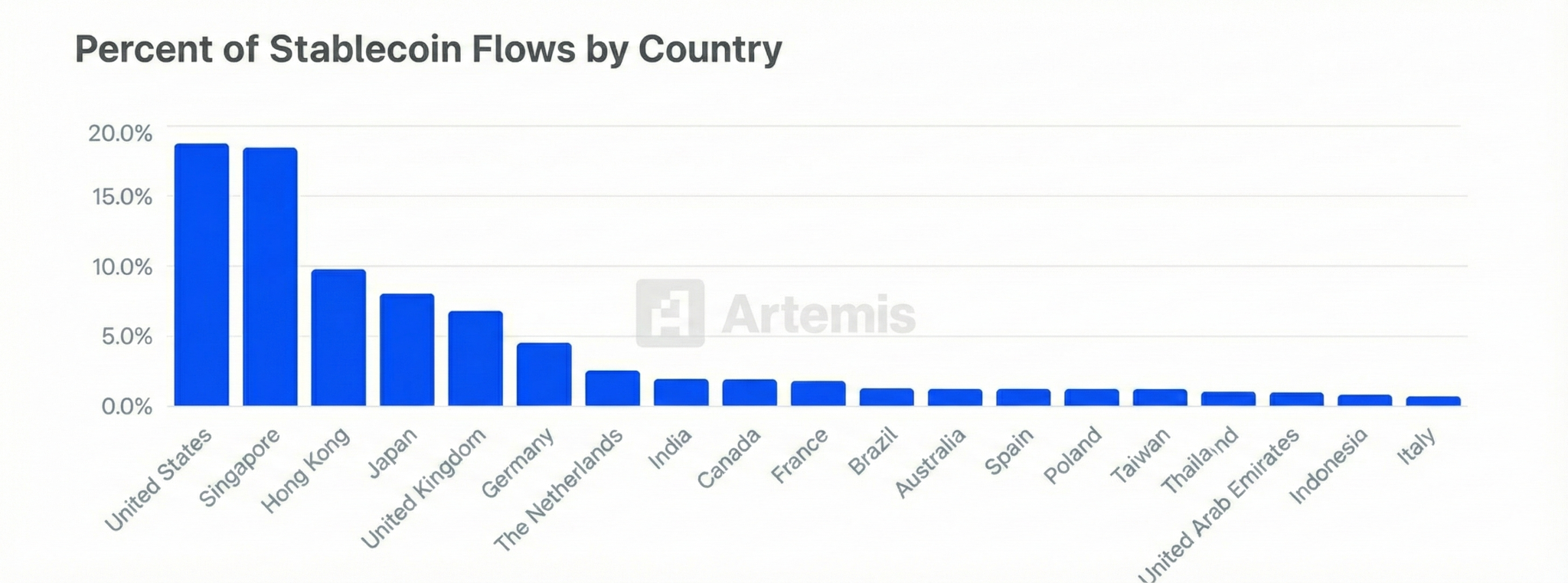

The United States, Singapore, Hong Kong, Japan, and the United Kingdom were the countries with the highest stablecoin transaction volumes.

How stablecoin connect to domestic payment local rails

The rise of stablecoins is evident, but it is essential to understand how they integrate with payment networks across different regions and enable faster and secure transactions.

Because they are anchored on a blockchain, stablecoins function as a neutral, global, and 24/7-available layer. This turns the blockchain into a universal rail capable of connecting infrastructures such as SEPA, Fedwire, CHAPS, and other domestic networks, allowing value to flow between them without the need for direct integrations or complex bilateral agreements.

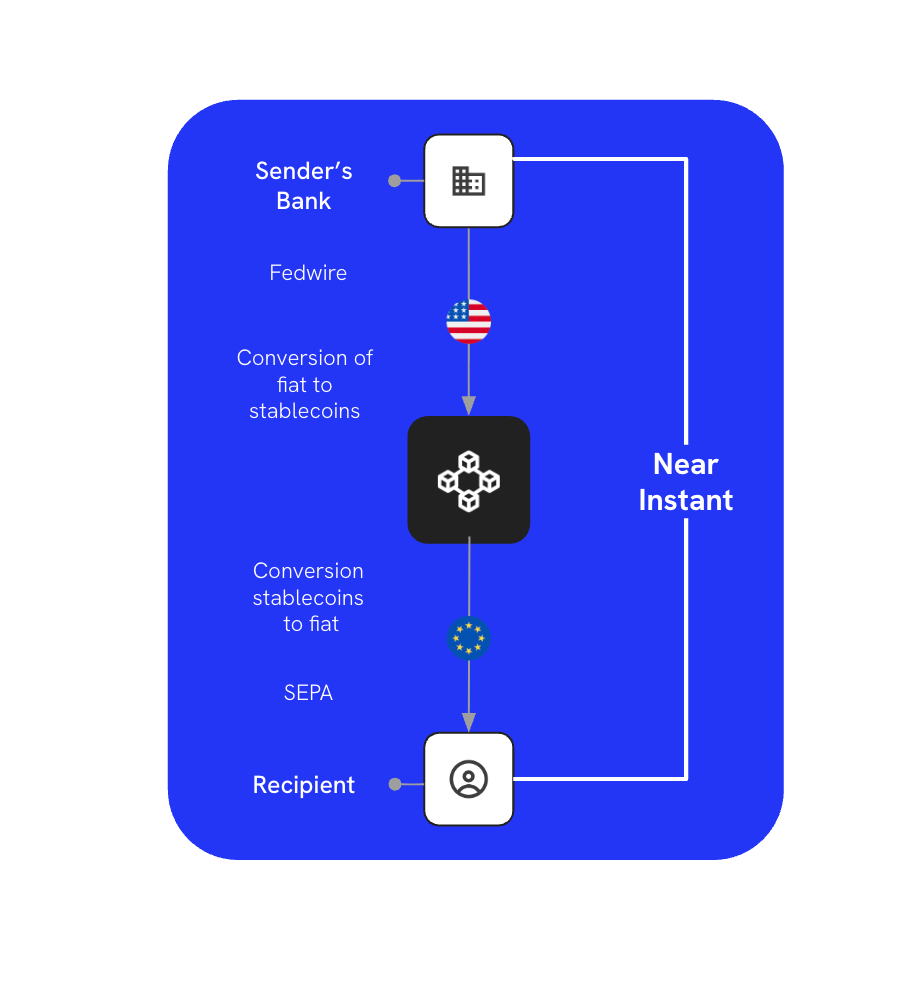

Here’s an example of how traditional and emerging technologies converge to enable faster and more efficient transactions. Conduit manages the on- and off-ramp conversion between fiat and stablecoins, with settlement flowing through the blockchain integrated into our infrastructure.

This model is possible because blockchains operate as global, borderless settlement infrastructures, while stablecoins provide a stable and interoperable asset that is not tied to any single jurisdiction. As a result, companies can settle funds in any domestic payment network using the same digital asset, simplifying processes, reducing costs, and accelerating global payments.

Like any cross-border transaction, stablecoin transfers comply with local regulations and incorporate standard international compliance and AML processes, including KYB, KYC, and transaction monitoring.

This represents a major improvement compared to legacy systems, where payments move through a fragmented network of correspondents, each with its own processes, timelines, and fees. These factors make international payment experiences opaque and unpredictable.

In this context, stablecoins emerge as an essential technology for an increasingly connected ecosystem, where economies, businesses, and individuals interact daily with agility, regardless of geographic borders.

As we look toward 2026 and the regulatory changes on the horizon, one thing is clear: the rise of stablecoins is not a temporary phase, but a structural shift that is here to stay.

Discover Conduit: The stablecoin infrastructure that connects local payment rails worldwide

The evolution of global payments requires more than fast domestic infrastructures. It demands a neutral, interoperable, always-on settlement layer capable of connecting fragmented payment systems across regions. Stablecoins provide exactly that missing layer, overcoming barriers that local rails were never designed to solve.

Conduit brings this new interoperable payment layer to businesses worldwide. Our stablecoin-powered platform connects companies to global money movement with real-time settlement, multi-currency capabilities, and seamless integrations with domestic rails.

If your business needs to move money across borders with the speed, efficiency and transparency of the digital era, Conduit is the infrastructure that makes it possible.

.jpg)

.jpeg)